Accounting For Managers Managerial Accounting

Question 1

Bonza Handtools Ltd. manufactures a popular power drill suitable for the home renovator. Financial and other data for this product for the last twelve months are as follows: Sales 20000 units

Selling price $130 per unit

Variable manufacturing cost $50 per unit

Fixed manufacturing costs $400000

Variable selling and administrative costs $30 per unit

Fixed selling and administrative costs $300000.

The directors of Bonza Ltd. want to try to increase the profitability of this product and invited senior staff to suggest how this might be done. Three suggestions have been received.

Give figures to support your comments and mention qualitative factors that may also be involved.

Direct Material Cost $2.50

Direct Labour Cost 3.00

Variable Factory Overhead 1.50

Fixed Factory Overhead 2.00

Manufacturing Cost 9.00

Variable Selling and Administrative Cost 2.00

Fixed Selling and Administrative Cost 1.50

Total Cost 12.50

20% Mark-up 2.50

Selling Price $15.00

The Company has an opportunity to bid for the supply of an additional 40000 units of its product to a government department. No sales commission (variable selling and admin. cost) is involved and no additional fixed costs will be incurred.

Give a reasoned opinion on the level of the bid that should be made in each of the following two circumstances

(i) The capacity of the Tassie Company's factory is 200000 units per year.

(ii) The capacity of the factory is only 180000 units per year.

Question 3

Critically discuss the following statements: Word limit for Question 3 - 750 words

Question 4

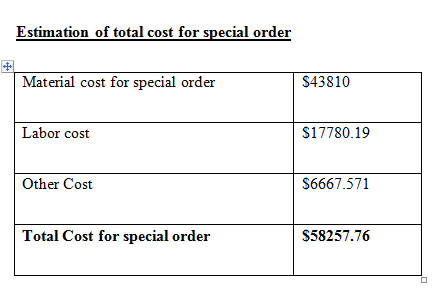

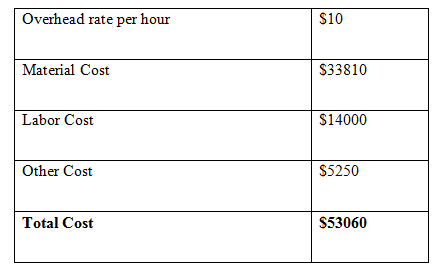

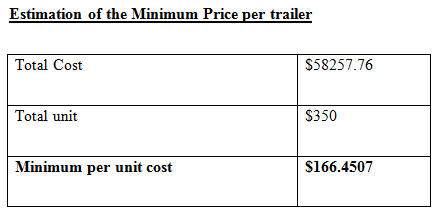

ABC Ltd makes trailers. It receives a special order to produce 350 trailers for a local retail outlet. The order will take 2,100 kg of material that costs $16.10 per kg and will require 1,400 direct labor hours and 525 machine hours. The following are the expected/budgeted annual costs for ABC Ltd:

Direct labour $327,600

Direct labor hours 25,795

Direct materials $193,200

Indirect costs $98,400

Machine hours 9,840

Required:-

Question 5

Write around 500 words explaining how segmenting the overheads can help in allocating overhead costs to individual jobs or services. You must support your discussion by real-world examples and acknowledge the source of your information (referencing).

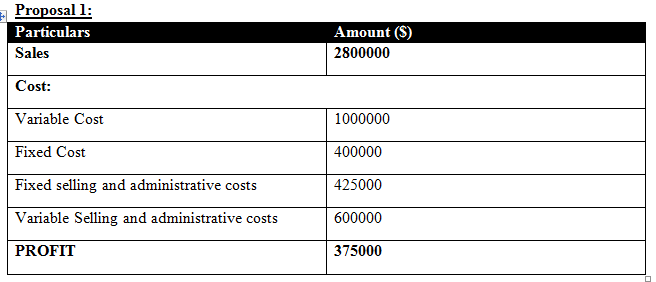

The above table demonstrated that if the first proposal is implemented, the organization will have a net profit of $375,000. Earlier, the net profit was estimated to be $300,000. Hence, the first proposal will help in increasing the profit level. However, it must be considered that the accountant has enhanced the selling price which might have a negative influence on the consumer perception regarding that product. Consequently, the demand may decline in long term (Fields, 2002).

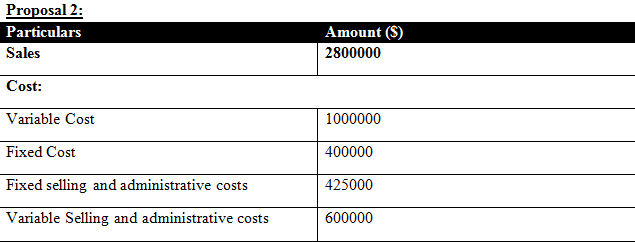

According to the production manager, profitability can be increased by focusing on quality control as well as promotional activities instead of increasing the selling price of the product. In this case, the profit has been estimated the same as the first proposal. However, significant risk is associated with this option as the result of the promotional strategy is uncertain (Epstein & Lee, 2011).

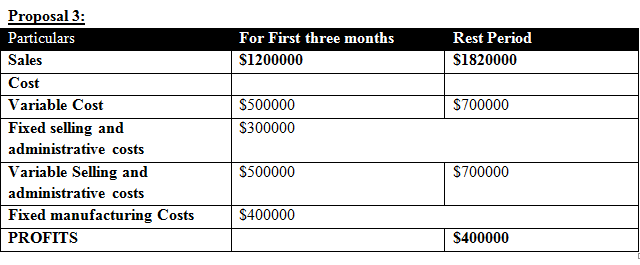

If the third proposal of the sales manager is implemented, the profit will be $400,000. In this strategy, the sales manager has focused on discount which will help in enhancing the sales volume. The decrease in the selling price will be compensated by the significant increase in the sales volume (Hansen & Mowen 2000).

Analyzing the three options, it can be stated that the third proposal is most appropriate for the company.

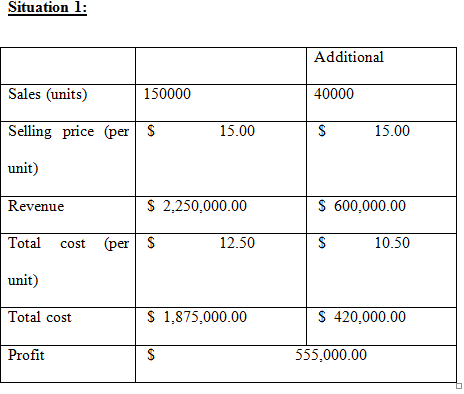

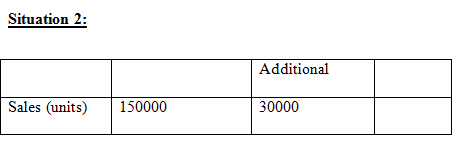

The above calculations depict that when the capacity of Tassie is 200,000 units per year and the profit will be estimated at $555,000. When the capacity of the factory will be 180,000 units per year the profit will be $ 510,000 (Dopson & Hayes 2009).

The management of an organization may analyze past trends in order to develop a new budget. Budget significantly contributes to monitoring the future operations of the company considering the budgeted figures as a basis of evaluation. It is necessary to adopt a flexible approach for preparing the budget as the real activities may deviate from the budgeted activities due to the change in circumstances (Gazely & Lambert 2006). It is important to prepare a realistic budget which considers provision for change in economic scenario or accidents. Positive variance with the budget demonstrates that the organization is performing effectively. On the other hand, negative variance clearly indicates the business firm has failed to operate effectively for meeting the minimum level of expectation (Fields, 2002).

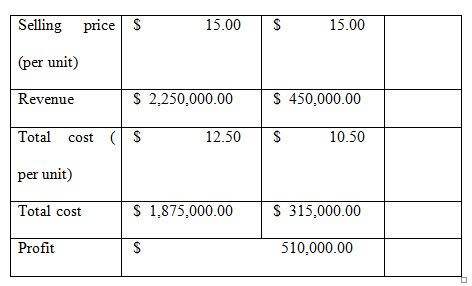

Estimation of cost of special order when machine time is considered as the base for allocating overheads

Segmented Overhead Cost and Activity-Based Budgeting

Segmented overhead expense helps in identification of the distinct variables as well as fixed costs related to manufacturing and operational activities which cannot be easily remembered in connection to the particular unit of the result. The segmented overhead cost can be distinguished with various operational assets such as a machine which is associated with the labor, setup cost etc. Therefore, a positive association can be established between real and standard expenditure. A segmented overhead cost includes different division of expenditure which can be associated with the cost of produced goods. Hence, it can help in the adoption of an effective pricing strategy (Collier, 2012).

Toyota has been adopted the procedure of segmenting overhead costs for enhancing the efficiency of the costing practice in the organization. Different overhead costs include indirect overhead, administrative overhead, selling overhead, manufacturing overhead etc. It is very important to identify properly the type of each cost and categorizing it properly. For instance, when a business firm is focusing on the classification of the different office supply, it must be included in the administrative overhead (Coombs, Hobbs & Jenkins 2005). Legal and accounting expenditures, auditing, office expenditures, audit fees etc will be categorized as the indirect overhead cost. The wages related to material handling, production supplies, the utility of the types of equipment will be considered as the variable overhead. Segmentation of the overhead costs significantly contributes to reducing the risk related to the overhead cost and undertakes the costing process efficiently (Gregoriou & Finch 2012).

Coombs, Hugh M, David Hobbs, and D. E Jenkins. 2005. Management Accounting. London: SAGE Publications.

Dopson, Lea R, & David K Hayes. 2009. Managerial Accounting For The Hospitality Industry. Hoboken, N.J.: John Wiley & Sons.

Epstein, Marc J, & John Y Lee. 2011. Advances In Management Accounting. Bingley, UK: Emerald.

Fields, E. (2002). The essentials of finance and accounting for nonfinancial managers. New York: AMACOM.

Gazely, Alicia M, & Michael Lambert. 2006. Management Accounting. London: SAGE Publications.

Gregoriou, Greg N, and Nigel Finch. 2012. Best Practices In Management Accounting. New York: Palgrave Macmillan.

Hansen, Don R, & Maryanne M Mowen. 2000. Management Accounting. Cincinnati: South-Western College Pub.

The Best Assignment help is one of the best website for assignment help. For more details, you may contact us at thebestassignmenthelp@gmail.com

managerial accounting

visit at: Auditing And Ethical Practice In Australia

Selling price $130 per unit

Variable manufacturing cost $50 per unit

Fixed manufacturing costs $400000

Variable selling and administrative costs $30 per unit

Fixed selling and administrative costs $300000.

The directors of Bonza Ltd. want to try to increase the profitability of this product and invited senior staff to suggest how this might be done. Three suggestions have been received.

- The accountant, Jan Rossi, believes that a price increase of $10 per unit is the best way to boost profits. She would spend an additional $125000 on national advertising and contends, that if this is done, sales volume would not drop appreciably from last year.

- The production manager, Tom Tune, thinks that an improved quality product could increase sales volume by 25% if accompanied by an advertising campaign costing $50000 aimed at tradespeople as well as home renovators. The improved quality would add $5 per unit to the variable cost. Mr. Tune believes that the price should not be increased.

- The sales manager, Mary Watson, wants to undertake a promotion campaign where a $10 rebate is offered on all drills sold during the three months beginning 1 April. Normally 6000 units are sold during that period and Ms. Watson believes that this could be boosted to 10000 units if an advertising campaign costing $40000 were launched late in March.

Give figures to support your comments and mention qualitative factors that may also be involved.

Question 2

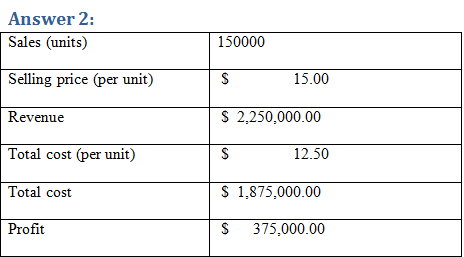

The Tassie Company estimates that next year it will manufacture and sell 150000 units of its product. On the basis of that level of activity, it has budgeted for the following costs and prices per unit:Direct Material Cost $2.50

Direct Labour Cost 3.00

Variable Factory Overhead 1.50

Fixed Factory Overhead 2.00

Manufacturing Cost 9.00

Variable Selling and Administrative Cost 2.00

Fixed Selling and Administrative Cost 1.50

Total Cost 12.50

20% Mark-up 2.50

Selling Price $15.00

The Company has an opportunity to bid for the supply of an additional 40000 units of its product to a government department. No sales commission (variable selling and admin. cost) is involved and no additional fixed costs will be incurred.

Give a reasoned opinion on the level of the bid that should be made in each of the following two circumstances

(i) The capacity of the Tassie Company's factory is 200000 units per year.

(ii) The capacity of the factory is only 180000 units per year.

Question 3

Critically discuss the following statements: Word limit for Question 3 - 750 words- ‘a budget is a forecast of what is expected to happen in business during the next year’

- ‘budgets are okay but they stifle all initiative. No manager would work for a business that applies control through budgets.’

- ‘any sensible person would start with the sales budget and build up the other budgets from there.’

- ‘a budget trying to be realistic will not motivate the best performance.’

- ‘only adverse variances are worth investigating, because favorable variances, by definition, must be good.’

Question 4

ABC Ltd makes trailers. It receives a special order to produce 350 trailers for a local retail outlet. The order will take 2,100 kg of material that costs $16.10 per kg and will require 1,400 direct labor hours and 525 machine hours. The following are the expected/budgeted annual costs for ABC Ltd:Direct labour $327,600

Direct labor hours 25,795

Direct materials $193,200

Indirect costs $98,400

Machine hours 9,840

Required:-

- Calculate the overhead allocation rate: note that the process is labor-intensive

- Calculate the total costs of the special order

- Calculate the cost of the special order if ABC Ltd uses machine time as the basis for allocating overheads

- Calculate the minimum price per trailer that ABC Ltd could accept.

- Explain how segmented overhead cost pools and activity-based costing can assist accurate costing for pricing purpose (200 words)

Question 5

Write around 500 words explaining how segmenting the overheads can help in allocating overhead costs to individual jobs or services. You must support your discussion by real-world examples and acknowledge the source of your information (referencing).Answer:

The above table demonstrated that if the first proposal is implemented, the organization will have a net profit of $375,000. Earlier, the net profit was estimated to be $300,000. Hence, the first proposal will help in increasing the profit level. However, it must be considered that the accountant has enhanced the selling price which might have a negative influence on the consumer perception regarding that product. Consequently, the demand may decline in long term (Fields, 2002).

According to the production manager, profitability can be increased by focusing on quality control as well as promotional activities instead of increasing the selling price of the product. In this case, the profit has been estimated the same as the first proposal. However, significant risk is associated with this option as the result of the promotional strategy is uncertain (Epstein & Lee, 2011).

If the third proposal of the sales manager is implemented, the profit will be $400,000. In this strategy, the sales manager has focused on discount which will help in enhancing the sales volume. The decrease in the selling price will be compensated by the significant increase in the sales volume (Hansen & Mowen 2000).

Analyzing the three options, it can be stated that the third proposal is most appropriate for the company.

The above calculations depict that when the capacity of Tassie is 200,000 units per year and the profit will be estimated at $555,000. When the capacity of the factory will be 180,000 units per year the profit will be $ 510,000 (Dopson & Hayes 2009).

Answer 3:

Budget is an important financial estimate for anticipating future requirements as well as the performance of the organization. The budget helps in forecasting the future requirement of capital by estimating sales volume, demand, and cost of manufacturing activities. Preparation of budget helps in effective allocation of the available resources (Epstein & Lee, 2009). The estimated profit from the budget helps in setting the target for the organizational performance and individual role of the employees for achieving it.The management of an organization may analyze past trends in order to develop a new budget. Budget significantly contributes to monitoring the future operations of the company considering the budgeted figures as a basis of evaluation. It is necessary to adopt a flexible approach for preparing the budget as the real activities may deviate from the budgeted activities due to the change in circumstances (Gazely & Lambert 2006). It is important to prepare a realistic budget which considers provision for change in economic scenario or accidents. Positive variance with the budget demonstrates that the organization is performing effectively. On the other hand, negative variance clearly indicates the business firm has failed to operate effectively for meeting the minimum level of expectation (Fields, 2002).

Answer 4

Estimation of cost of special order when machine time is considered as the base for allocating overheads

Segmented Overhead Cost and Activity-Based Budgeting

Segmented overhead expense helps in identification of the distinct variables as well as fixed costs related to manufacturing and operational activities which cannot be easily remembered in connection to the particular unit of the result. The segmented overhead cost can be distinguished with various operational assets such as a machine which is associated with the labor, setup cost etc. Therefore, a positive association can be established between real and standard expenditure. A segmented overhead cost includes different division of expenditure which can be associated with the cost of produced goods. Hence, it can help in the adoption of an effective pricing strategy (Collier, 2012).

Answer 5:

Segmenting overhead is an important aspect for allocation of the overhead cost as it provides support in identification of the cost associated with setting up, material purchase, operation, and inspection (Dopson & Hayes 2009).Toyota has been adopted the procedure of segmenting overhead costs for enhancing the efficiency of the costing practice in the organization. Different overhead costs include indirect overhead, administrative overhead, selling overhead, manufacturing overhead etc. It is very important to identify properly the type of each cost and categorizing it properly. For instance, when a business firm is focusing on the classification of the different office supply, it must be included in the administrative overhead (Coombs, Hobbs & Jenkins 2005). Legal and accounting expenditures, auditing, office expenditures, audit fees etc will be categorized as the indirect overhead cost. The wages related to material handling, production supplies, the utility of the types of equipment will be considered as the variable overhead. Segmentation of the overhead costs significantly contributes to reducing the risk related to the overhead cost and undertakes the costing process efficiently (Gregoriou & Finch 2012).

References

Collier, Paul M. 2012. Accounting For Managers. Chichester, U.K.: Wiley.Coombs, Hugh M, David Hobbs, and D. E Jenkins. 2005. Management Accounting. London: SAGE Publications.

Dopson, Lea R, & David K Hayes. 2009. Managerial Accounting For The Hospitality Industry. Hoboken, N.J.: John Wiley & Sons.

Epstein, Marc J, & John Y Lee. 2011. Advances In Management Accounting. Bingley, UK: Emerald.

Fields, E. (2002). The essentials of finance and accounting for nonfinancial managers. New York: AMACOM.

Gazely, Alicia M, & Michael Lambert. 2006. Management Accounting. London: SAGE Publications.

Gregoriou, Greg N, and Nigel Finch. 2012. Best Practices In Management Accounting. New York: Palgrave Macmillan.

Hansen, Don R, & Maryanne M Mowen. 2000. Management Accounting. Cincinnati: South-Western College Pub.

The Best Assignment help is one of the best website for assignment help. For more details, you may contact us at thebestassignmenthelp@gmail.com

managerial accounting

visit at: Auditing And Ethical Practice In Australia

No comments:

Post a Comment